{kind=link}

The principles of the Difference Between Avoidable and Unavoidable Cost are broadly discussed all around the globe. There are several variations between your avoidable and unavoidable cost. Avoidable cost can be segregated in changing costs, displayed in inputs of labor, capital, and natural materials, and stepped set costs, symbolized in investment necessary to change the total degree of output of the company. Unavoidable costs are segregated in expense resulted of organized risk and changes in capital cost for evaluating the business. The primary representations of avoidable cost are displayed in labor cost, natural materials costs and capital costs that can purchase in local or international marketplaces depending on the comparative price of inputs. Unavoidable costs are exogenous to stable and there is a consequence of organized risk cost of capital, and professional performance.

Comparison Table “Avoidable Cost and Unavoidable Cost”

| Velocity: | It could be excluded as consequence of velocity of development. | It is out there even if creation is not performed. |

| Separation: | These are immediate costs for the company. | They are indirect costs for the company. |

| Management | There is manipulated by the company. | Influenced by exterior affairs from the company. |

| Swap | Costs can be acquired and turned in the market of multiple providers from local and abroad roots. | Occurs when only can be found a service provider of special service to operate the company or produced at a commercial level. |

| Short Fall of Revenue | Related to inputs for development. | Associated with the opportunity of use of capital and organized risk. |

Brief Explanation Avoidable Cost VS. Unavoidable Cost

What is Avoidable Cost?

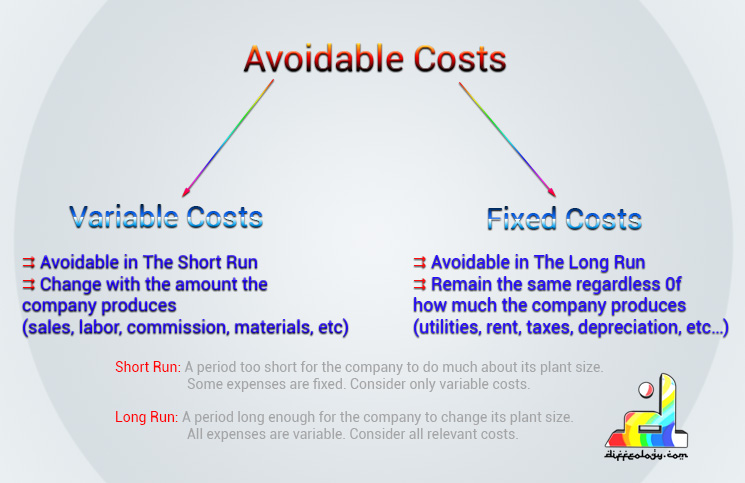

It’s the cost incurred only when firm requires a decision related to development or investment is considered. This type of cost is adjustable and is determined by the level of productivity and by exterior inputs where the organization may take choice depending on an expense of opportunity for multiple decisions and bonuses.

An avoidable cost is an expense that may be removed by not participating in or no more performing a task. For example, if you opt to close a creation line, then the expense of the building where it is housed is currently an avoidable cost because you can sell the building. The avoidable cost notion is essential when participating in cost decrease activities.

Over the future, all costs are avoidable. For example, a 25 years rent is avoidable if the decision-making period is more than 25 years. For a while, legally-mandated or government-mandated costs, such as leases or environmental cleanup commitments, aren’t avoidable costs. Generally, a changing cost is known as to be an avoidable cost, while a set cost is not regarded as an avoidable cost. In the short-term, many costs are believed to be set and for that reason unavoidable.

Also Read: Idle Cost and Standard Cost How To Differentiate

From a risk management point of view, it pays to regularly review the price structure of the business and make an effort to shift as much costs as is feasible from the unavoidable to the avoidable category, gives management increased room to go if the business enterprise suffers an earnings shortfall and must scale back on its expenditures. For example, a rent can be restored with a shorter term, so that management gets the option to cancel the related charge in a shorter time frame than had recently been the situation. As known in the example, the overall strategic method of coping with avoidable costs is to invest in shorter schedules for any organized expenditures.

Similar Terms

“An avoidable cost is also called an escapable cost.”

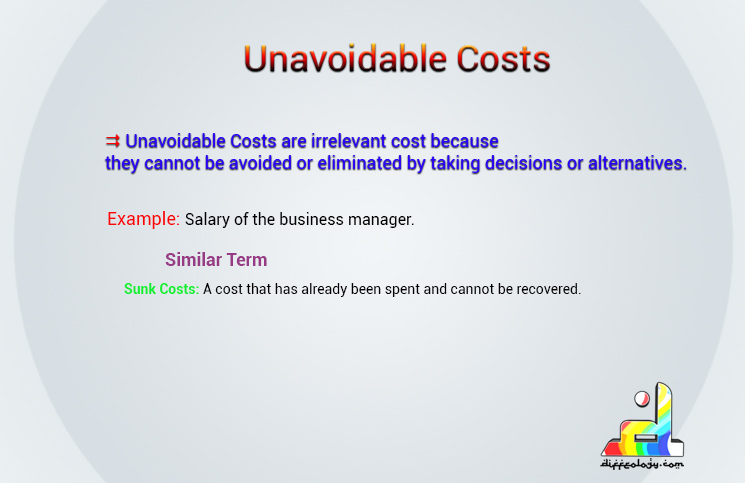

What is Unavoidable Cost?

It’s the cost that still incurred for the organization even if the decision of producing is not used. These costs are the consequence of risk considered by organizations in their business for maintaining on the market and cover doubt of decisions of creation. The set cost is the key representation of unavoidable cost for organizations, as consequence of firm to set up capacity, administrative labor force and tools, require a short investment you can use or possibly not. Types of unavoidable costs send circumstances where quality will depend on a single supplier of a source with a distinctive quality of product impact over costs of the company. This type of cost can’t be managed by the company and averted unless organization get new providers and turn it into an avoidable cost.

Also Read: Difference Between Lending Rate and Borrowing Rate

Additional types of unavoidable costs happen when organized risk of going for a position of financial investments impact adversely over come back of organization, and can’t be protected with the diversification of investment.

Similar Terms

Sunk Costs: “A cost that has already been spent and cannot be recovered.”

Differences Between Avoidable and Unavoidable Cost In Detail

Here are some of the major differences between avoidable and unavoidable cost.

Speed of production

- The consumption of labor, capital, and uncooked material inputs count of the degree of production made a decision to undertake for the organization.

- The unavoidable costs do not rely upon the velocity of creation, but it occurs as a short investment to operate the firm.

Managing costs

- The avoidable cost can be handled by firm scheduled to it is determined by an even of output described by a search engine optimization criterion, being income maximization or decrease costs.

- The organization cannot control it as consequence of exogenous variables took place at macroeconomic and professional level.

Swap

- Firms can move avoidable costs in the market, using local or international providers of inputs necessary to create last product.

- The organization cannot turn unavoidable costs in the market as result it generally does not have immediate substitutes but evaluating the changes made in the costs.

Revenue brief fall

- In the case of avoidable cost, if the company cannot achieve maximization earnings, can make move towards a posture of minimizing costs and steer clear of cost related to the creation, where average cost and marginal cost have the same

- As consequence of the reduced amount of benefits made by the business, unavoidable cost related capital cost, organized risk, default risk and coverage of adversity cost may increase.

Conclusion: Avoidable and Unavoidable Cost

Avoidable and Unavoidable Cost are the two terms that are related to business’s theory for valuation and take on the decision of development of the firm. Avoidable costs symbolize the inputs where the organization can transform it depending on multiple degrees of production. Unavoidable costs signify costs where it generally does not rely upon the velocity of creation and organization cannot control by organized risk and economic conditions.

Avoidable cost is divided in changing cost that changes on discrete worth and stepped set cost that changes on businesses decision to increase installed capacity and degrees of outcome beyond its limit.

Avoidable and unavoidable cost can be evaluated at current prices and differentiate them, to financial commitment and success of the business.